MCF Weekly Capital Market Review - October 14th, 2019

Trump teased the public over the weekend on the US-China trade deal, saying “Good things are happening” and that the deal is the greatest and biggest for US farmers. More details were released Sunday with Trump introducing phases for the trade deal. Phase One involves China immediately purchasing “very large quantities” of US agricultural product. The reported range is $40-$50 billion, which would about double the 2017 level of US agricultural exports to China.[1] In return, the US will keep tariff rates at 25% (rather than raising to 30% as scheduled for October 15) on $250 billon of Chinese goods.[2] There are no details of Phase Two or its contents, much less the number of phases and respective timelines. If Phase One turns out to be true, even partially, it would be a positive episode in the long and continuing saga of the US-China trade war.

Brexit will likely be back in the news by the end of week as Prime Minister Boris Johnson has until October 19th to deliver a Brexit deal approved by Parliament. If not, he would be legally required to request an extension from the EU.[3] Losing three Brexit deal votes and extending the deadline twice effectively ended the PM tenure of Johnson’s predecessor Theresa May, who was forced out by the Tory party as a result. Johnson ran a hardline campaign for PM promising to deliver Brexit by October 31 and wishes to avoid a similar fate as May. There is little talk surrounding the details of a deal, so businesses and investors are still left guessing. Odds place a 28% chance of Brexit being cancelled altogether.[4]

Powell announced that the Fed will soon expand its balance sheet.[5] In reality, the balance sheet reached an inflection point at the end of August and has expanded since the beginning of September.[6] Monetary expansion is the Fed’s plan going forward, but Powell admonished that policy is not preset. The Fed will continue to be data dependent and will likely change depending on an array of financial and economic factors. Given softer inflation data and weakening economic outlook, especially globally, a lot of positive news would be required to reverse course.

CPI was softer than expected with a year-over-year reading of 1.7%; producer prices were even softer at 1.4%. Weakness in labor markets is starting to show with the JOLTS job openings and new hires both falling more than expected. Economic indicators were not all negative as consumer sentiment enjoyed a nice bounce since last month.

This week’s releases will include retail sales, the Beige book, and several Fed member speeches.

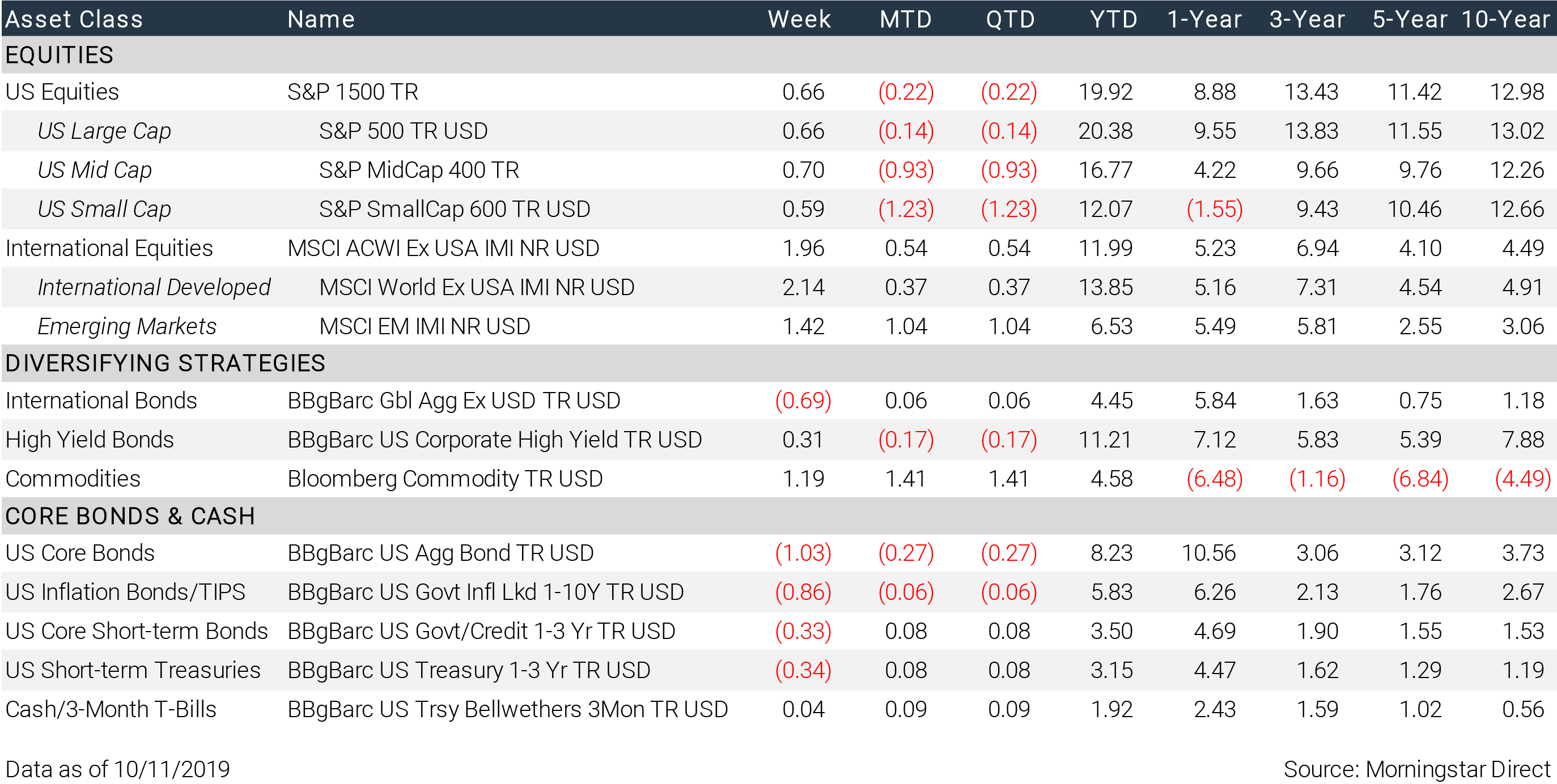

INDEX RETURNS

[1] https://www.reuters.com/article/us-usa-trade-china-agriculture/trumps-hailing-of-50-billion-in-chinese-farm-purchases-seen-as-meaningless-idUSKBN1WT0TG

[5] https://markets.businessinsider.com/news/stocks/federal-reserve-powell-says-balance-sheet-expansion-will-start-soon-2019-10-1028585021

[6] https://fred.stlouisfed.org/series/WALCL

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by MCF), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from MCF. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. MCF is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of the MCF’s current written disclosure statement discussing our advisory services and fees is available upon request. If you are an MCF client, please remember to contact MCF, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services. Please click here to review our full disclosure.

REFLECTED INDICES

S&P Composite 1500® Index combines three leading indices, the S&P 500®, the S&P MidCap 400®, and the S&P SmallCap 600® to cover approximately 90% of the US market capitalization. It is designed for investors seeking to replicate the performance of the US equity market or benchmark against a representative universe of tradable stocks. Investors cannot invest in an index.

MSCI ACWI ex USA Index captures large and mid cap representation across 22 of 23 Developed Markets (DM) countries (excluding the US) and 23 Emerging Markets (EM) countries. With 1,859 constituents, the index covers approximately 85% of the global equity opportunity set outside the US. Investors cannot invest in an index.

Bloomberg Barclays Global Aggregate ex-USD Index is a measure of global investment grade debt from 24 local currency markets. This multi- currency benchmark includes treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging markets issuers. Investors cannot invest in an index.

Bloomberg Barclays High Yield Corporate Bond Index measures the USD-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody's, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on Barclays EM country definition, are excluded. Investors cannot invest in an index.

S&P GSCI is a composite index of commodity sector returns which represents a broadly diversified, unleveraged, long-only position in commodity futures. The S&P GSCI is intended to provide exposure to broad-based commodities. Investors cannot invest in an index.

Bloomberg Barclays US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed- rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass- through), ABS and CMBS (agency and non-agency). Provided the necessary inclusion rules are met, US Aggregate eligible securities also contribute to the multi-currency Global Aggregate Index and the US universal Index, which includes high yield and emerging markets debt. The US Aggregate Index was created in 1986 with history backfilled to January 1, 1976. Investors cannot invest in an index.

Bloomberg Barclays 1-10 Year US Government Inflation-Linked Bond Index tracks the 1-10-year inflation protected sector of the United States Treasury market. Investors cannot invest in an index.

Bloomberg Barclays US Treasury 1-3 Year Index measures the performance of public obligations of the US Treasury with maturities of 1-3 years, including securities roll up to the US Aggregate, US Universal, and Global Aggregate Indices. Investors cannot invest in an index.

Bloomberg Barclays US Treasury Bellwethers 3 Month Index is an unmanaged index representing the on-the-run (most recently auctioned) US Treasury bill with 3 months’ maturity. Investors cannot invest in an index.